FIRE Retirement and new IRIS system

On June 16, 2023, we informed that the IRS plans to retire the Filing Information Returns Electronically ("FIRE") platform for electronic transmission of 1042-S and 1099 Forms and replace it with the Information Returns Intake System (“IRIS”). Recently, the IRS specified that, starting with filing season 2027 (for tax year 2026 onwards), the FIRE platform will be retired. Therefore, the IRIS platform will be the only system used to file information returns.

Within the FIRE system, Forms 1042-S and 1099 are currently submitted using a .txt file format, while the IRIS system requires filings the respective reportings as a CSV file through the taxpayer portal (limited to a maximum of 100 forms) or as an .xml file using the A2A (Application-to-Application) platform, which allows for the submission of more than 100 forms. Form 8809, used to request more time to file information returns, will be also submitted through IRIS.

Withholding Agents planning on uploading CSV files for 1042-S and 1099 reporting can find the formatting rules on the IRS website.

Publication 5717 provides guidance on registering for a TCC to electronically submit information returns via IRIS. The roles available for selection are as follows:

Issuer - to be chosen if the taxpayer is submitting its own information returns through the portal

Transmitter - to be used for third parties transmitting in the name of taxpayers through the portal (and A2A platform if the transmitter has acquired the Software Developer role as well)

Software Developer – to be used if Forms are to be filled through the A2A platform

The roles are not mutually exclusive, i.e. a taxpayer may apply for several roles with the IRS. As per Publication 5903, two responsible officials (“RO”) must be appointed for the application purposes. Before filing the application, the RO must be authenticated through ID.me, obtain a valid ITIN or SSN and provide confirmation that they are a U.S. citizen. A RO can appoint further authorized users to use the IRIS platform.

Currently, as already experienced with the “IR for TCC” system, IRIS appears to be unavailable to individuals who are not citizens of the United States.

IRIS is enabled for the filing of Forms 1099 for tax year 2022 and later and for the filing of Forms 1042-S for tax year 2025 and later. With the announced retirement of FIRE in 2027, it remains unclear if amendments of Forms 1042-S (for tax year 2025 and previous years), whose original filing was submitted through FIRE, and new Forms 1042-S (for tax year 2025 and previous years) can be submitted through IRIS after December 31, 2026. Currently, the IRS is working on a process for corrections in IRIS for previous tax years.

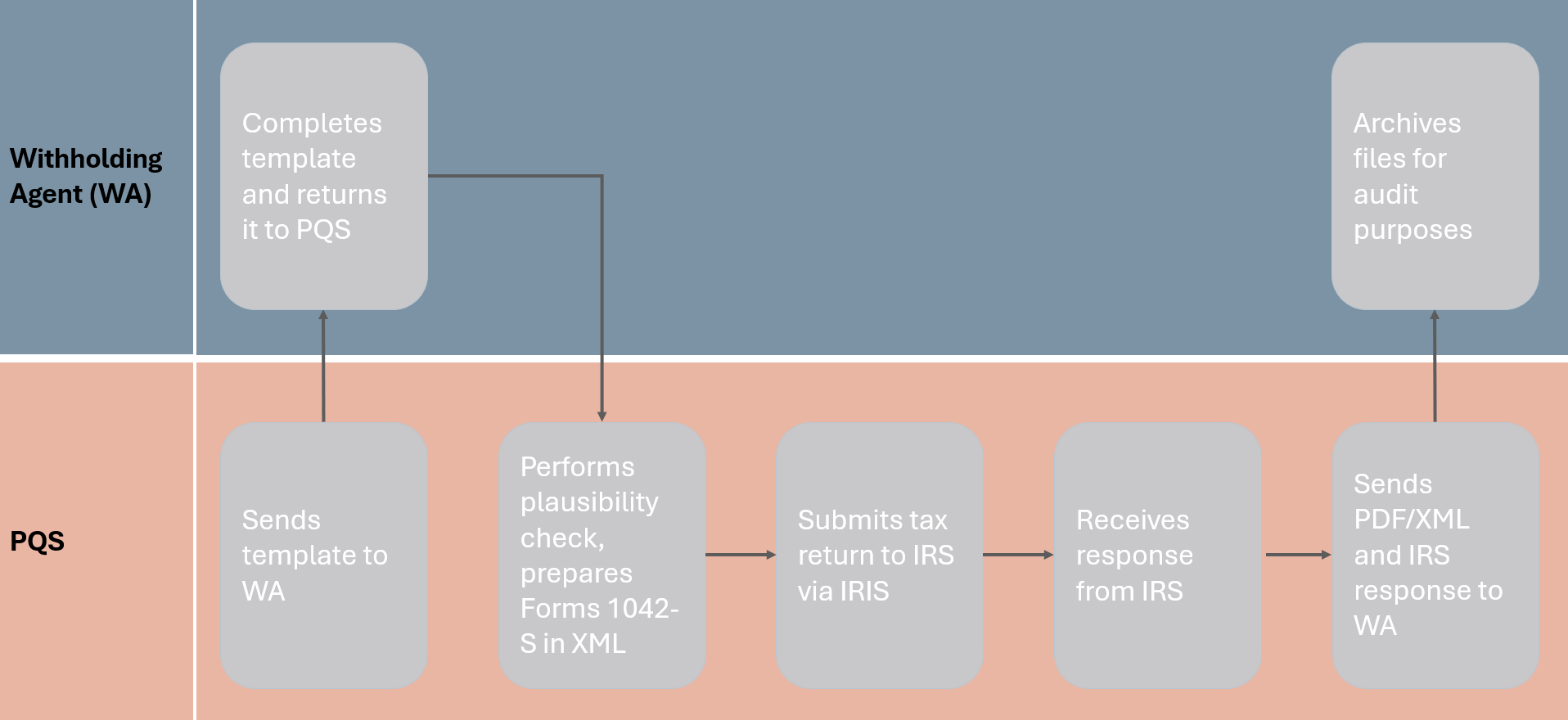

Due to upcoming changes in the electronic filing obligations for Forms 1042-S and 1099, PQS has obtained Transmitter and Software Provider status with the IRS and is now able to file these forms via the Information Returns Intake System (“IRIS”). In this capacity, PQS can assist QIs, QDDs, WFPs, WFT and other withholding agents in complying with their filing obligations and in submitting requests for extensions of time to file (Form 8809) through IRIS.

Our IRIS solution entails:

the submission of the request of time extension for filing Forms 1042-S and 1099 via IRIS (Form 8809),

the validation of the template filled out by the withholding agent,

the generation of the Forms 1042-S and Forms 1099 as xml-file and .pdf (Recipient Copies B, C and D) according to the template,

the submission of the information return to the IRS with our IRIS login via the A2A platform, and

the forwarding of the submitted Forms as .xml-file and .pdf (Recipient Copies B, C and D) and of the IRS response as xml-file.

If you are interested in engaging us for this service, please contact us. If you are already a valued client of our services, we will contact you within the next weeks separately.